Example Applications

This section documents some of the applications that SurPyval as a survival analysis toolkit can be useful to you, no matter what discipline you need it for.

Boston House Prices

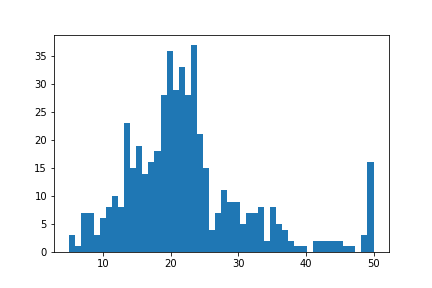

No statistical analysis package can avoid doing the ‘hello world’ task of analysing the ‘Boston House Pricing’ dataset. What might surprise some readers is that this would even be considered… The myriad blogs and Kaggle posts looking into this problem can not surely be improved upon. I agree, however, it is a good example of why one needs to be aware of censoring and how flexible the SurPyval API is when dealing with it. Looking at the boston house pricing dataset you can see that there is a suspicous number of houses at the top end that all have the same price:

On consideration, one can see that there are no houses above $50,000 and that the density at that point is much higher than we would expect because we would expect some form of a ‘fat-tail.’ That is, we should expect a decreasing number of houses at the highest costs. It is therefore safe to conclude that all values above $50,000 have been set to $50,000; which is to say that the sale price is right censored! And because it is a censored observation we will need to use an analysis tool that can handle censored observations, lest we may be wrong in our estimates of the distribution of housing prices. So lets load the data and see what results we can get, starting with the raw data.

import surpyval as surv

from surpyval.datasets import load_boston_housing

x = load_boston_housing()['medv'].values

x, c, n, _ = surv.xcnt_handler(x)

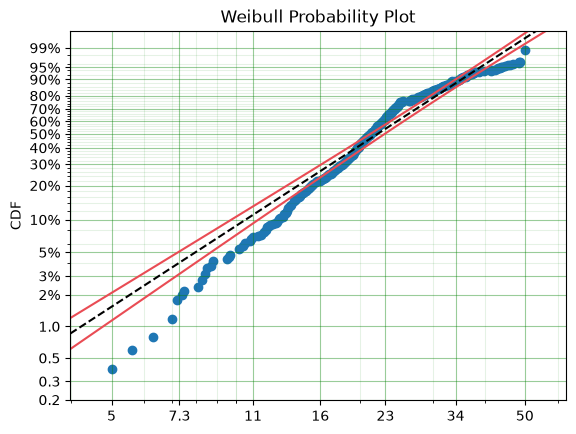

model = surv.Weibull.fit(x, c, n)

print(model)

model.plot()

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Parameters :

alpha: 25.38695283239701

beta: 2.5651903209947626

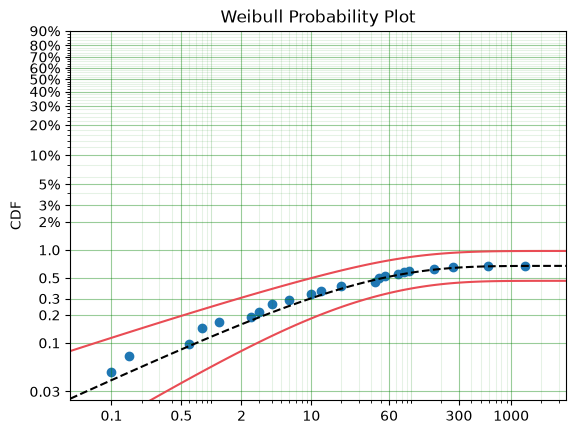

<Axes: title={'center': 'Weibull Probability Plot'}, ylabel='CDF'>

From the above plot you can see that near 50, the parametric model diverges substantially from the actual data. So we can see that having not censored the highest values means that our model could be improved by doing so. Let’s see:

import surpyval as surv

from surpyval.datasets import load_boston_housing

x = load_boston_housing()['medv'].values

x, c, n, _ = surv.xcnt_handler(x)

# Right censor the highest value

c[-1] = 1

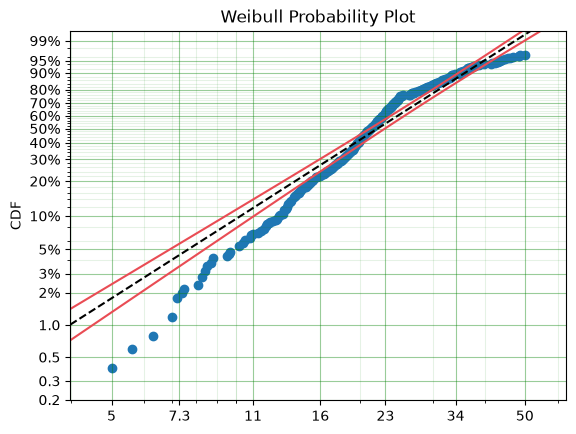

model = surv.Weibull.fit(x, c, n)

print(model)

model.plot()

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Parameters :

alpha: 25.536696019933206

beta: 2.469159446459558

<Axes: title={'center': 'Weibull Probability Plot'}, ylabel='CDF'>

We can see that the model has changed slightly, however, there appears to be a ‘disconnect’ near 24 that makes the model a poor fit above and below the value. Let’s see if a different distribution will improve the fit:

import surpyval as surv

from surpyval.datasets import load_boston_housing

x = load_boston_housing()['medv'].values

x, c, n, _ = surv.xcnt_handler(x)

# Right censor the highest value

c[-1] = 1

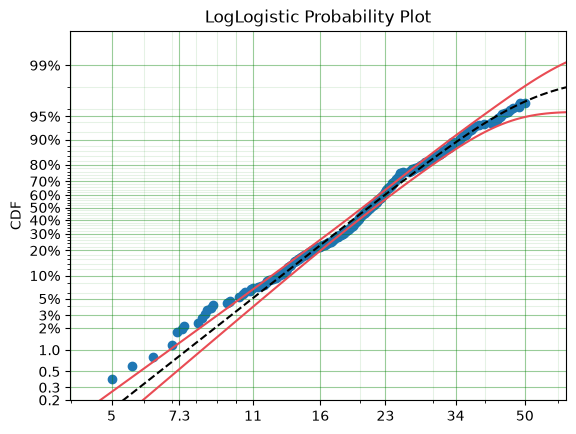

model = surv.LogLogistic.fit(x=x, c=c, n=n, lfp=True)

print(model)

model.plot()

Parametric SurPyval Model

=========================

Distribution : LogLogistic

Fitted by : MLE

Max Proportion (p) : 0.986113385277025

Parameters :

alpha: 20.80440553057851

beta: 4.561905097771235

<Axes: title={'center': 'LogLogistic Probability Plot'}, ylabel='CDF'>

This appears to be a much better fit, however, there is still quite a bit of difference between the data and the model in the middle of the distribution. Lets create a custom spline to see if we can perfect the fit.

import surpyval as surv

from surpyval.datasets import load_boston_housing

from autograd import numpy as np

x = load_boston_housing()['medv'].values

x, c, n, _ = surv.xcnt_handler(x)

# Right censor the highest value

c[-1] = 1

def Hf(x, *params):

x = np.array(x)

Hf = np.zeros_like(x)

knot = params[0]

params = params[1:]

dist1 = surv.Weibull

dist2 = surv.LogLogistic

Hf = np.where(x < knot, dist1.Hf(x, *params[0:2]), Hf)

Hf = np.where(x >= knot, (dist1.Hf(knot, *params[0:2])

+ dist2.Hf(x, *params[2::])), Hf)

return Hf

bounds = ((0, 50), (0, None), (0, None), (0, None), (0, None),)

param_names = ['knot', 'alpha_w', 'beta_w', 'alpha_ll', 'beta_ll']

name = 'WeibullLogLogisticSpline'

support = (0, np.inf)

WeibullLogLogisticSpline = surv.CustomDistribution(name, Hf, param_names, bounds, support)

model = WeibullLogLogisticSpline.fit(x=x, c=c, n=n, lfp=True)

print(model)

model.plot()

Parametric SurPyval Model

=========================

Distribution : WeibullLogLogisticSpline

Fitted by : MLE

Max Proportion (p) : 0.9710331348405039

Parameters :

knot: 25.300000000010197

alpha_w: 23.011773691993547

beta_w: 3.8753626468925417

alpha_ll: 32.50093514004742

beta_ll: 10.339766491173446

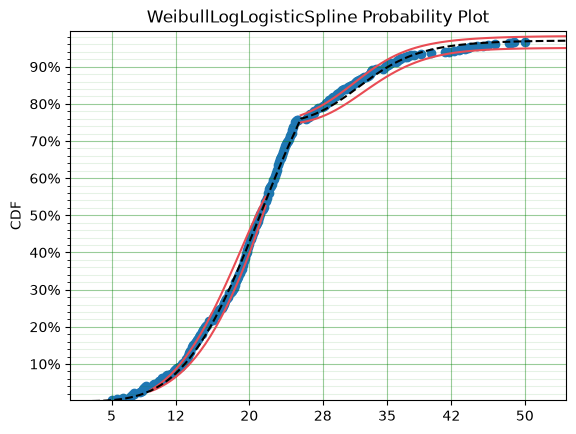

<Axes: title={'center': 'WeibullLogLogisticSpline Probability Plot'}, ylabel='CDF'>

Much better!

It must be said that this is a bit ‘hacky’. There is no theory that we are using to guide the choice of the spline model, we are simply finding the best fit to the data. For example, this model would not able to be used for extrapolation too far beyond $50,0000, this is because the model is limited to 97.1% of houses. A separate spline would be needed to model those data. However, the example shows the importance of censoring and the power of the surpyval API!

Applided Reliability Engineering

In reliability engineering we might be interested in the proportion of a population that will experience a particular failure mode. We do not want to ship the items that will fail so that our customers do not have a poor experience. But, we will want to determine the minimum duration of a test that can establish whether a component will fail. This is because a test that is too long we will waste time and money in testing and if a test is too short we will ship too many items that will fail in the field. We need to optimise this interval the minimize the cost of testing but also the number of items at risk in the field.

Using data from the paper that introduced the Limited Failure Population model (also known as the Defective Subpopulation) to the reliability engineering world [Meeker] we can show how surpyval can be used in part to calculate an optimal ‘burn-in’ test duration.

import surpyval as surv

f = [.1, .1, .15, .6, .8, .8, 1.2, 2.5, 3., 4., 4., 6., 10., 10.,

12.5, 20., 20., 43., 43., 48., 48., 54., 74., 84., 94., 168., 263., 593.]

s = [1370.] * 4128

x, c, n, _ = surv.fs_to_xcnt(f, s)

model = surv.Weibull.fit(x, c, n, lfp=True)

print(model)

model.plot()

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Max Proportion (p) : 0.0067444509491608184

Parameters :

alpha: 28.36719792750094

beta: 0.4959762213659723

<Axes: title={'center': 'Weibull Probability Plot'}, ylabel='CDF'>

We can see from these results that at maximum we will have approximately 0.67% fail. If the company accepts a 0.1% probability of their products failing in the field then we can calculate the interval at which the difference between the total population and the proportion failed in the test is 0.1%.

from scipy.optimize import minimize

fun = lambda x : (0.001 - np.abs(model.p - model.ff(x)))**2

res = minimize(fun, 10, tol=1e-50)

print(res.x)

[104.43742685]

Therefore we should do a burn in test up to approximately 104.4 to make sure we minimize the number of items shipped that are defective while also minimizing the duration of the test. We can simply change the value of 0.001 in the above code to any value we may wish to use.

Demographics / Actuarial

In demographics and actuarial studies, the distribution of the life of a population is of interest. For the demographer, it is necessary to understand how a population might change, in particular, how the expected lifespan is changing over time. The same applies to an actuary, an actuary is interested in lifetimes to understand the risk of payouts among those who own a life insurance policy.

The Gompertz-Makeham is a distribution used in demography and actuarial studies to estimate the lifetime of a population. This can be implemented in surpyval with relative ease.

import surpyval as surv

from autograd import numpy as np

from matplotlib import pyplot as plt

from scipy.special import lambertw

bounds = ((0, None), (0, None), (0, None),)

support = (0, np.inf)

param_names = ['lambda', 'alpha', 'beta']

def Hf(x, *params):

Hf = params[0] * x + (params[1]/params[2])*(np.exp(params[2]*x))

return Hf

GompertzMakeham = surv.CustomDistribution('GompertzMakeham', Hf, param_names, bounds, support)

We now have a GM distribution object that can be used to fit data. But we need some data:

# GM qf()

def qf(p, params):

lambda_ = params[0]

alpha = params[1]

beta = params[2]

return (alpha/(lambda_ * beta) - (1./lambda_)*np.log(1 - p)

- (1./beta)*lambertw((alpha*np.exp(alpha/lambda_)*(1 - p)**(-(beta/lambda_)))/(lambda_))).real

np.random.seed(1)

params = np.array([.68, 28.7e-3, 102.3])/1000

x = qf(np.random.uniform(0, 1, 10_000), params)

# Filter out some numeric overflows.

x = x[np.isfinite(x)]

/tmp/ipykernel_825/341577025.py:7: RuntimeWarning: overflow encountered in power - (1./beta)*lambertw((alpha*np.exp(alpha/lambda_)*(1 - p)**(-(beta/lambda_)))/(lambda_))).real /tmp/ipykernel_825/341577025.py:7: RuntimeWarning: invalid value encountered in multiply - (1./beta)*lambertw((alpha*np.exp(alpha/lambda_)*(1 - p)**(-(beta/lambda_)))/(lambda_))).real

The parameters for the distribution come from [Gavrilov], specifically the parameters for the lifespans of the 1974-1978 data. So in this case we have (simulated) data on the lifespans of 10,000 people and we need to determine the GM parameters. This can be compared to the historic parameters to see if the age related mortality has changed or has remained roughly constant. To do so, all we need do with surpyval is to put the data to the fit() method.

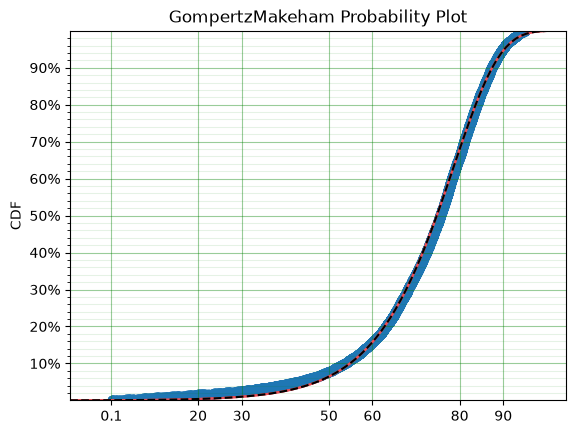

model = GompertzMakeham.fit(x)

model.plot(alpha_ci=0.99, heuristic='Nelson-Aalen')

model

Parametric SurPyval Model

=========================

Distribution : GompertzMakeham

Fitted by : MLE

Parameters :

lambda: 1.0805709794454957e-12

alpha: 5.590567530354162e-05

beta: 0.09452891507420386

You can see that the model is a good fit to the data. Using the model we can determine the probability of death in a given term for a random individual from the population. This is useful to price the premium of a life insurance policy. For example, if a 60 year old was to take out a two year policy, what premium should we charge them for the policy. First, we need to determine the probability of death:

p_death = model.ff(62) - model.ff(60)

policy_payout = 100_000

expected_loss = policy_payout * p_death

print(p_death, expected_loss)

0.029581699513831272 2958.169951383127

From the results above, you can see that the probability of death over the two year interval is approximately 2.5%. Given the contract is to payout $100,000 in this event, the expected loss is therefore $2,548.32. Therefore, to make a profit, the policy will need to cost more than $2,548.32. So say the company has a strategy of making 10% from each policy, the policy cost to the individual would therefore be $2,803.15. If we divide this payment scheme into a per month basis over the two years we get a monthly payment of $116.80 for two years (in the case of death the amount owing can be subtracted from the payout).

Although this is a basic example, as insurance companies would have much more sophisticated models, it shows the basics of how demographic and actuarial data can be used. This shows the application of surpyval to actuarial and demogrphic studies.

Applied Reliability Engineering - 2

In reliability engineering you can come across the case where a new product has been built that is similar in design to a previous, but has better materias, geometry, seals.. etc. You have data from the tests of the old product and new results for the same test on the new product. The only problem, the new product only had one failure in the test! What will you do?

Given the similarities, it is common to use the same shape parameter, the \(\beta\) value, from a similar product as an initial estimate. In this case, we may need to know the reliability of the item in the field. We can create a model of this new product, but first the old product:

import surpyval as surv

x_old = [ 5.2, 10.7, 16.3, 22. , 32.9, 38.6, 42.1, 58.7, 92.8, 93.8]

old = surv.Weibull.fit(x_old)

print(old)

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Parameters :

alpha: 45.27418430640352

beta: 1.3776233667367648

We can use the above value of beta with the new data:

x_new = [87, 100]

c_new = [0, 1]

n_new = [1, 9]

surv.Weibull.fit(x_new, c_new, n_new, fixed={'beta' : 1.3776}, init=[100.])

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Parameters :

alpha: 525.2284054870862

beta: 1.3776

The characteristic life of the new bearing is over 10 times higher! Quite an improved new design. This new model can be used as part of the sales of the new product (10x more life!) and to provide recommendations for maintenance.

Economics

Economists are interested in the times between recessions. This information helps them formulate policy proscriptions that may (or may not) reduce the duration of a recession, or the time between recessions. Using data from Tadeu Cristino et al. [TC] we can use real data to esimate the probability of a recession.

import pandas as pd

import surpyval as surv

start = [np.nan, "June 1857", "October 1860", "April 1865", "June 1869",

"October 1873", "March 1882", "March 1887", "July 1890", "January 1893",

"December 1895", "June 1899", "September 1902", "May 1907", "January 1910",

"January 1913", "August 1918", "January 1920", "May 1923", "October 1926",

"August 1929", "May 1937", "February 1945", "November 1948", "July 1953",

"August 1957", "April 1960", "December 1969", "November 1973",

"January 1980", "July 1981", "July 1990", "March 2001", "December 2007"]

end = [

"December 1854", "December 1858", "June 1861", "December 1867", "December 1870",

"March 1879", "May 1885", "April 1888", "May 1891", "June 1894", "June 1897",

"December 1900", "August 1904", "June 1908", "January 1912", "December 1914",

"March 1919", "July 1921", "July 1924", "November 1927", "March 1933",

"June 1938", "October 1945", "October 1949", "May 1954", "April 1958",

"February 1961", "November 1970", "March 1975", "July 1980", "November 1982",

"March 1991", "November 2001", "June 2009"

]

df = pd.DataFrame({'start' : pd.to_datetime(start),

'end' : pd.to_datetime(end)})

# Compute time from end of last recession to peak of next.

x = (df.start - df.end.shift(1)).dropna().dt.days.values

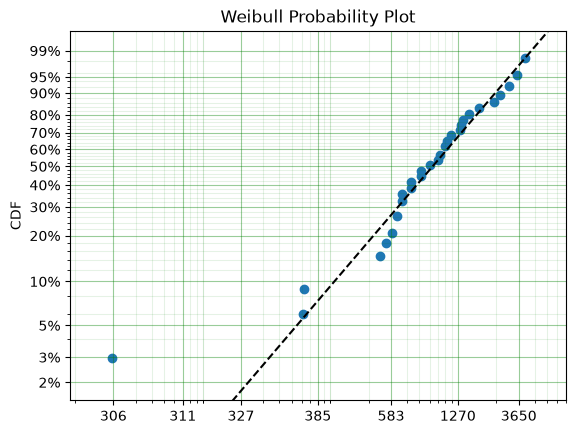

model = surv.Weibull.fit(x, offset=True)

print(model)

model.plot()

/tmp/ipykernel_825/566552608.py:23: UserWarning: Could not infer format, so each element will be parsed individually, falling back to `dateutil`. To ensure parsing is consistent and as-expected, please specify a format.

df = pd.DataFrame({'start' : pd.to_datetime(start),

/tmp/ipykernel_825/566552608.py:24: UserWarning: Could not infer format, so each element will be parsed individually, falling back to `dateutil`. To ensure parsing is consistent and as-expected, please specify a format.

'end' : pd.to_datetime(end)})

Parametric SurPyval Model

=========================

Distribution : Weibull

Fitted by : MLE

Offset (gamma) : 304.06590396747373

Parameters :

alpha: 895.3220827750343

beta: 1.062949129835668

<Axes: title={'center': 'Weibull Probability Plot'}, ylabel='CDF'>

You can see from the above the data is a good fit to the model! Great. So now what?

We can communicate what the expected time between recessions is:

model.mean()

np.float64(1178.2499324754347)

Therefore the average growth period is 1,178 days, or about 3.2 years between recessions.

References

- TC

Tadeu Cristino, C., Żebrowski, P., & Wildemeersch, M. (2020). Assessing the time intervals between economic recessions. PloS one, 15(5), e0232615.

- Duwe

Duwe, G., Sanders, N. E., Rocque, M., & Fox, J. A. (2021). Forecasting the Severity of Mass Public Shootings in the United States. Journal of Quantitative Criminology, 1-39.

- Gavrilov

Gavrilov, L. A., Gavrilova, N. S., & Nosov, V. N. (1983). Human life span stopped increasing: why?. Gerontology, 29(3), 176-180.

- Meeker

William Q. Meeker (1987) Limited Failure Population Life Tests: Application to Integrated Circuit Reliability, Technometrics, 29(1), 51-65

Social Science / Criminology

Another application of surpyval is when encountering extreme values. The Weibull distribution is one of the limiting cases of the Generalized Extreme Value distribution. In other words, the Weibull distribution is the distribution that can model the strength of a chain because it can model the extreme value, in this case the minimum, of a collection of distributions. A chain is as only as strong as it’s weakest link. If there are many many links in a chain (which is a fair assumption) then links of which follow a known strength distribution, then the strength of the chain will will follow a Weibull distribution. It is for this reason that the Weibull distribution is so widely used.

Another extreme value is the maximum. The maximum extreme value distribution is the Frechet distribution. But, if you simply inverse a minimum, you can get a maxmimum. Therefore, if we know our data is following a process of finding a maximum, then we can use the Weibull distribution to model the phenonmena.

Warning

This may be a distressing topic for some readers.

Social scientists and criminologists are interested in understanding the phenomena of mass shootings in an effort to eliminate the scourge from society. A mass shooting is an extreme event, and an extreme event can be modelled to understand the risks of future occurence, and with that understanding, the effect of interventions can also be understood.

Using the gun violence data from Kaggle we can model the process. That is, if we take the maximum number of deaths in a given month over several years, we have data that can be used to estimate the probability of something even worse occuring. This data covers the period from 2013 to 2018, see Kaggle for more details.

It is worth reminding that since we have taken the inverse, it is the lower values that represent more victims. And it is the extremes that we are trying to capture. You can see from the above plot that the model does not fit the data from 0.02 to 0.1 very well. We can try using a different approach

You can see that this model is a much better description of the data. However, the problem is that it cannot have a real interpretation. Because the offset is negative, that means there is a non-zero probability of 0, which because the data was inversed, means that there is a non-zero probability of having a shooting with infinite victims. This model is therefore not a good option for such extreme extrapolations. The model can however, be used to estimate the probabiltiy of having a shooting as bad or worse than the most extreme event up to 2040.

The model estimates that there is an approximately 1.6% chance of an event killing 50 or more people in a given month, which may seem low, however, because there are 216 months between 2022 and 2040 the chances of not having as extreme an event over that time period becomes horrifyingly small. The model suggests that the probability of having a month in which an event with more than 50 people will be killed, has a 97.0% chance of happening from 2022 to 2040. Chilling.

This is a bit higher than other reports of the same prediction, see [Duwe] who report at 35% probability, which is some, but not even close to complete, relief.